The advisory role in internal audit

We are currently witnessing a growing trend in internal audit functions including more advisory engagements in their audit plans.

We are aware that in accordance with the standards of the Institute of Internal Auditors (IIA), it is perfectly permissible to carry out this type of engagement provided it is disclosed in the internal audit charter. Why, then, are many functions still reluctant to perform advisory engagements? What benefits are to be gained from this type of engagement?

First, it should be noted that advisory engagements require somewhat different skills and abilities than traditional assurance engagements. Both the Internal Audit Manager and members of the team should adopt a “business advisor” approach toward the organization rather than an “auditor” approach. The following attributes[1] are required for this type of engagement:

- Intellectual curiosity and open‑mindedness

- Leadership and dynamic communication skills

- Desire to work collaboratively with others

- Critical judgment, diplomacy and persuasion skills

In addition, by analyzing the current internal audit market and exchanging with a number of internal audit managers, it is clear that the concepts of independence and objectivity are still very often key concerns with respect to advisory engagements. It should be noted here that the auditor’s ability to engage in advisory activities without impairing their independence depends to some extent on the distinction they make between assisting or consulting in an advisory role versus an execution role, which is management’s responsibility. As a result, internal audit functions must develop procedures to analyze advisory engagements and determine whether they pose a threat to their independence and objectivity. The review carried out to determine the effect on independence and objectivity should be properly documented. The documentation should be available at the time of the external quality assessment in connection with the quality assurance and improvement program.

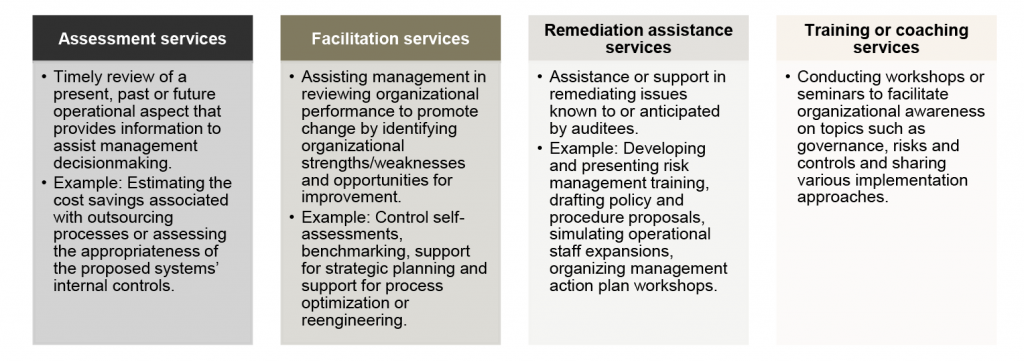

Most internal audit functions that have reached a certain level of advisory maturity offer the following services.[2] The ultimate goal is certainly to communicate the advisory services offered within the organization and position internal audit as a key player in achieving organizational goals.

What are the expected benefits?

- Increased credibility of the internal audit function within the organization

- More specific knowledge of organizational processes (operational and strategic)

- Perception of value added for stakeholders

- New skills developed for the internal audit team and broader expertise

- Positioning the internal audit function as a key player in the organization

Why start now?

Our current reality and the need for a forward‑looking approach indicate that tomorrow’s organizations will have to be more agile to remain relevant. Advisory engagements will clearly be in greater demand from internal audit functions. For organizations contemplating a transformation, such as adopting more computerized, automated and secure processes, who better than internal audit to support them along the way?

There is no question that internal audit functions will have to facilitate their transition from a traditional audit role to a more agile support and advisory role. We are reminded that internal auditors are among the few actors with cross‑cutting knowledge of the organization they work for. The time is ripe to show and express their desire to contribute!

Richter can help with:

- Diagnostic of the internal audit function

- Preparation of a hybrid internal audit plan (assurance and advisory)

- Designing support for the advisory service offering

- Benchmarking

- Contribution of best practices and current trends

- Training, working sessions and facilitation of workshops on the advisory role

[1] SOURCE: TRUSTED ADVISORS: KEY ATTRIBUTES OF OUTSTANDING INTERNAL AUDITORS.

[2] SOURCE: APPLYING THE INTERNATIONAL PROFESSIONAL PRACTICES FRAMEWORK, 4TH EDITION.