M&A Lookback on the North American Food Sector 2025

2025 M&A Lookback

Transaction Overview of the North American Food Sector

M&A activity in the North American food sector remained selective throughout 2025, shaped by cautious buyer behavior amid continued macroeconomic and policy uncertainty.

Timing and fit emerged as the primary drivers of unsuccessful transactions this year. As part of our 2025 North American Food Sector Survey, Richter surveyed over 150 executives from private middle value chain food companies. Nearly half of those who engaged in M&A discussions but did not complete a transaction cited economic uncertainties and strategic alignment as the main reasons deals did not proceed. The negotiation process, while still a challenge for operators, was a lesser concern in 2025, with 31% fewer respondents identifying it as the primary reason for an unsuccessful outcome.

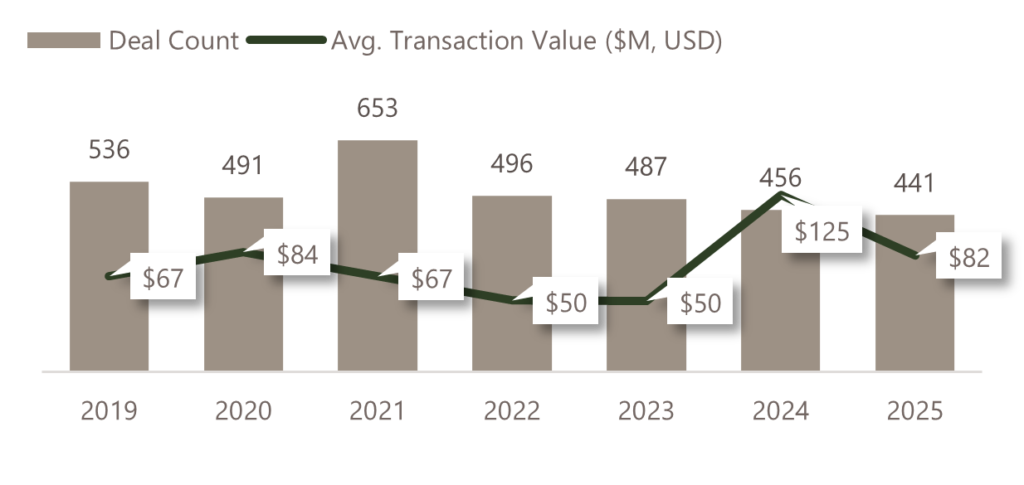

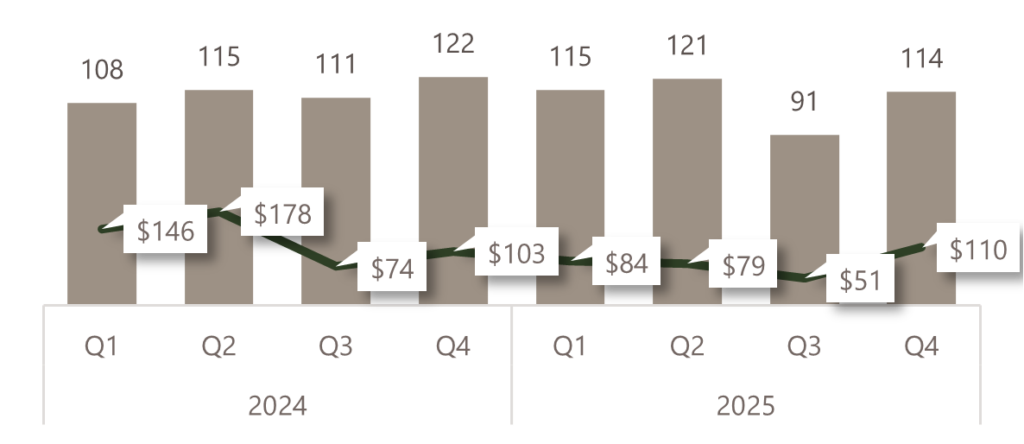

This sentiment was reflected in the quarterly pattern of M&A activity observed in 2025. Total reported deal count declined to 441 transactions, with average disclosed transaction value decreasing to approximately $82 million for the year. Activity was relatively stable in the first half—Q1 and Q2 recorded 115 and 121 transactions, respectively, at average values of $84 million and $79 million—before a pronounced slowdown in the third quarter.

Q3 2025 saw deal volume fall to 91 transactions and average transaction value decline to $51 million, driven by heightened tariff and trade uncertainty that delayed buyer decisions and extended diligence timelines. As market conditions stabilized, activity rebounded in Q4, with 114 transactions and a recovery in average transaction value to approximately $110 million, signaling renewed buyer engagement toward year-end.

The fourth-quarter recovery was further underscored by several notable, large-scale transactions. In December 2025, Richardson International acquired Ronzoni for approximately $375 million, highlighting continued strategic interest in scaled, branded staple food platforms with established North American distribution. Earlier in the quarter, Wonder Group acquired Spyce for approximately $186 million, reflecting ongoing investor appetite for technology-enabled and innovation-driven food concepts that align with evolving consumer preferences and operational efficiency initiatives.

North American Food Sector M&A Transactions [1], [2] 2019-2025

Reported Deals in Capital IQ & Pitchbook

[1] Food industry defined as Food Distributors and Food Products (excluding Animal Feed) within Pitchbook and Capital IQ databases. Beverages are excluded. [2] Average transaction value excludes deals with no disclosed value (i.e., $0) and only considers transactions valued below $500M.

Sources: Pitchbook, Capital IQ

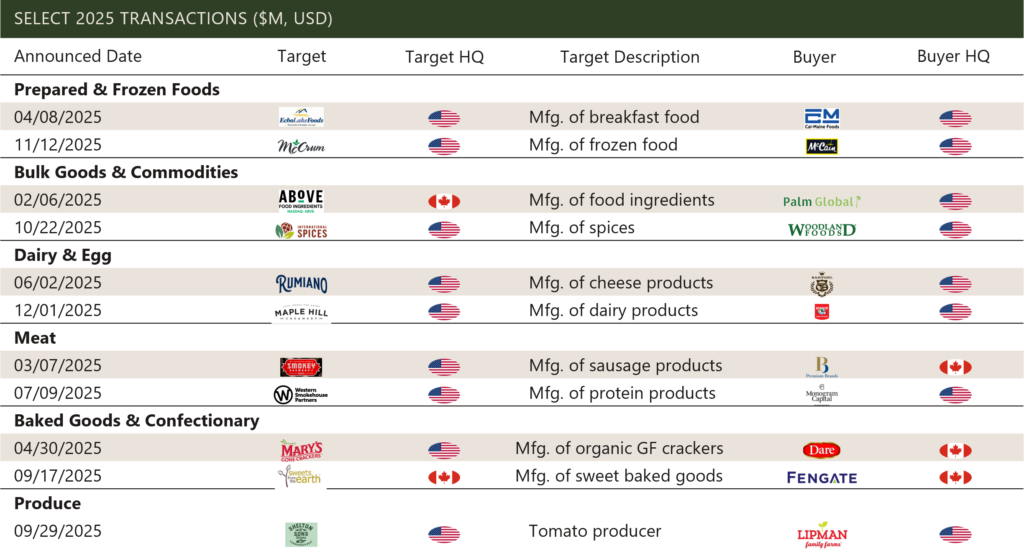

Notable Transactions in the North American Food Sector

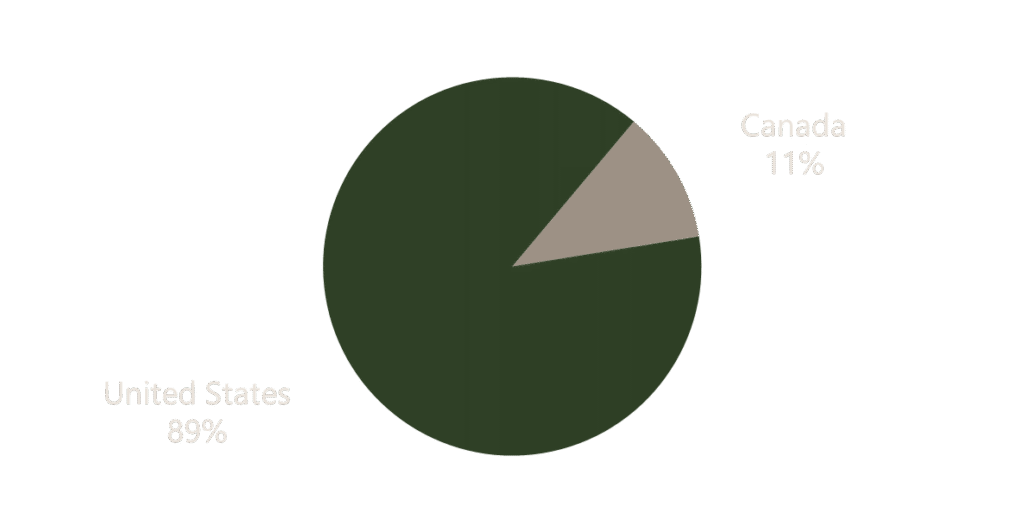

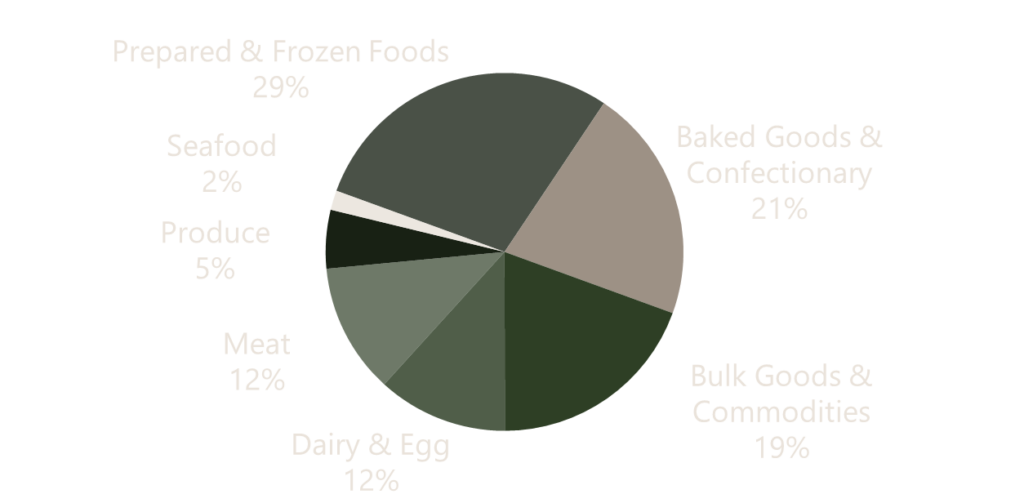

In 2025, North American food transactions were predominantly concentrated in the US, with the prepared and frozen foods, and baked goods and confectionary sectors experiencing highest activity.

2025 North American Food Transactions[1], By Country

2025 North American Food Transactions[2], By Segment

[1] Data from Pitchbook and Capital IQ. [2] CapitalIQ data only.

Sources: Pitchbook, Capital IQ

Valuation Trends in Private Equity-Backed M&A in North America

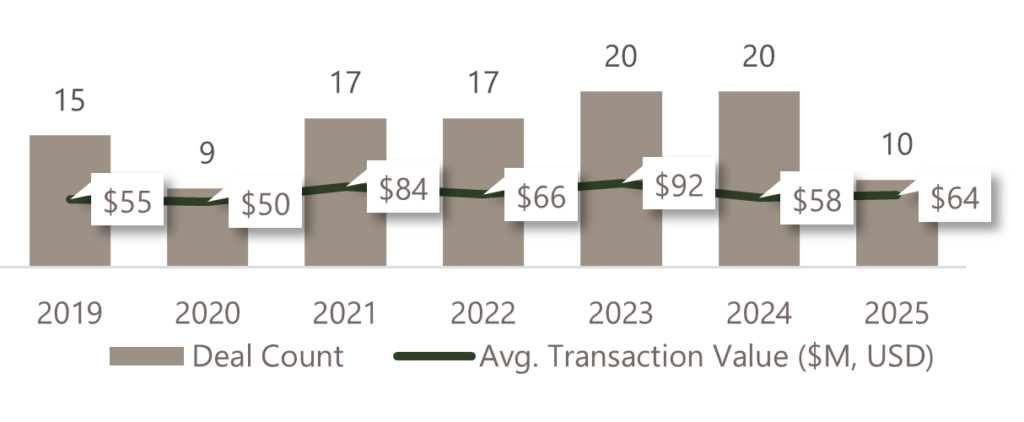

Private equity-backed M&A in the North American food sector remained selective in 2025, with 10 reported transactions and an average disclosed transaction value of approximately $64 million. This represents a moderation from 2023 and 2024, where 20 transactions were recorded each year, reflecting a more cautious deployment of capital amid continued valuation discipline and heightened underwriting standards.

Select Private Equity-Backed Company Food M&A [1], [2] Transactions, 2019-2025

Reported Deals in GF Data with disclosed valuation multiples

Select Private Equity-Backed Food Manufacturing, Wholesale and Distribution Multiples ($M, USD), 2019-2025[1], [2]

Reported Deals in GF Data with disclosed valuation multiples

| BY YEAR | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| TRANSACTION | 15 | 9 | 17 | 17 | 20 | 20 | 10 |

| AVG TEV | 54.9 | 49.5 | 83.9 | 65.8 | 91.9 | 57.9 | 63.6 |

| TEV/REV | 1.1x | 1.1x | 1.5x | 1.6x | 1.1x | 1.3x | 1.6x |

| TEV/EBITDA | 7.1x | 7.0x | 7.8x | 9.1x | 7.7x | 8.0x | 7.5x |

| BY TEV (PAST 7 YEARS) | $10-25M | $25-50M | $50-100M | $100-500M |

| TRANSACTION | 25 | 30 | 31 | 22 |

| AVG TEV | 18.0 | 36.4 | 67.0 | 174.1 |

| TEV/REV | 1.3x | 1.0x | 1.4x | 1.7x |

| TEV/EBITDA | 7.1x | 6.9x | 7.8x | 9.8x |

[1] NAICS 311 (excluding animal feed) and 4244 in GF Data. [2] 2025 data may not reflect all transactions, as deals continue to be added to the database.

Sources: GF Data

Despite lower deal volume, valuation multiples remained relatively stable, with TEV/EBITDA averaging 7.5x in 2025, broadly in line with long-term historical ranges. The data suggests that buyers continue to place a premium on high-quality, well-positioned assets, even as overall transaction activity softened.

By deal size, larger transactions command higher valuation premiums, with enterprises in the $100–500 million TEV range achieving average TEV/EBITDA multiples of approximately 9.8x, compared to 7.1x–7.8x for smaller transactions below $100 million. This aligns with our 2025 survey findings, where respondents identified channel penetration, product and capacity expansion, and the addition of new capabilities as the most attractive attributes in an acquisition target.

The premium also reflects the value placed on scale, platform readiness, and more institutionalized operating frameworks, including established management teams, formalized succession planning, and robust financial reporting systems, within the food manufacturing, wholesale, and distribution segments.