The Richter Economic Timeline: What was known or knowable and what did the market say?

Sources: Available upon request

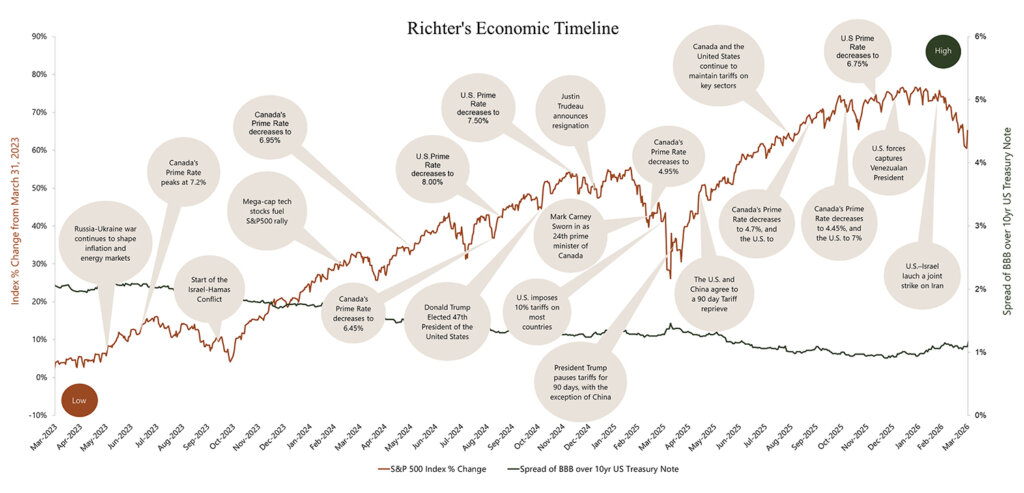

Richter’s economic timeline plots local and world events together with a depiction of the volatility of the stock market (S&P 500) and credit markets (the spread of publicly traded BBB corporate bonds over U.S. treasury notes).

Following record highs at the end of 2025, U.S. equities experienced a significant sell-off in Q1 2026. The S&P 500 posted its worst quarterly performance since 2022, dragged down by a sharp decline in mega-cap technology stocks, the outbreak of the U.S.-Iran war in late February, surging oil prices, and continued trade policy uncertainty. Central banks on both sides of the border held rates steady as they weighed the risks of an energy-driven inflation shock against softening labor markets. This occurred contemporaneously with the following:

- The S&P 500 posted its worst quarterly performance since 2022, declining approximately 4.4%, driven by geopolitical tensions, elevated oil prices, and waning AI enthusiasm.

- Canada’s unemployment decreased in January 2026, before rebounding to December 2025 levels in February and remaining flat in March, reflecting a softening in labour market conditions. Meanwhile, the U.S. unemployment rate fell slightly to 4.3%.

- Canada’s housing market remained soft through Q1 2026, with the National Composite MLS Home Price Index down 4.8% year over year as of February.

- In February, the U.S. Supreme Court struck down the use of International Emergency Economic Powers Act (IEEPA) to impose tariffs, prompting the administration to replace prior tariffs on non-CUSMA Canadian goods with a temporary 10% global import surcharge under Section 122.

- The Consumer Price Index (CPI) in Canada rose 1.8% in February year-over-year, following a 2.3% increase in January, partly reflecting base-year effects from the 2025 GST/HST break.

- On January 3, U.S. forces captured Venezuelan President Nicolás Maduro in a military operation in Caracas. Maduro and his wife were transferred to New York to face narco-terrorism and drug trafficking charges, drawing widespread international debate over the legality of the action.

- On February 28, the United States and Israel launched a joint military operation against Iran, describing it as a response to an imminent nuclear and security threat. This has resulted in a surge of global energy prices and a dampened outlook for economic growth.

This timeline was compiled by Richter Inc.’s Business Valuation and Dispute. A similar version was published in the CBV Institute’s Journal Advisory Group.

Link: https://cbvinstitute.com/wp-content/uploads/2020/11/CBV-Institute_Journal2020_Final.pdf